#finance

Penguins Refuse to Eat Cheaper #Fish After #Aquarium Cut Cost to Fight #Inflation

#watch: https://www.youtube.com/watch?v=Vd9vDVP28h8

#japan #news #penguin #costs #finance

4 Likes

1 Comments

#Inflation in the U.S. explained ...

watch: https://www.youtube.com/watch?v=MBo4GViDxzc

#economy #prices #politics #money #education #finance #news

5 Likes

1 Comments

how the modern fiat money system works - what causes inflation?

first of: “economics” is where “believe” and “science” meet.

Often it is not clear, what parts of economics is “real science” and what is “make believe”.

What is for sure: all “modern” monetary systems are FIAT systems,

this means, some entity (state or bank, usually “independent” bank of banks)

- prints an undefined amount of money (cash)

- as much as it deems to achieve it’s goals

- goals could be:

- 0% unemployment

- 2% inflation

- reversal of climate change

- peace & prosperity for all or just for the top 0.1%

- what have you

- goals could be:

- as much as it deems to achieve it’s goals

- it loans/lends that cash to private banks

- the private banks are (supposed) to lend to productive citizens, that actually give the money it’s value, by adding value to society

- by designing, building, creating, (mass) production of clever, innovative products & services that help people

- stay alive & healthy - clean water & food - healthcare

- get to work or to visit someone - transport

- communicate - phones, computers, wires that connect computers…

- by designing, building, creating, (mass) production of clever, innovative products & services that help people

- the private banks are (supposed) to lend to productive citizens, that actually give the money it’s value, by adding value to society

So ask yourself: What gives money it’s value?

As it has no intrinsic value (it is not gold and since the 70s the US-$ is (thanks to Nixon and the Vietnam war) not linked to gold anymore).

The German Mark after ww2 was one of the first FIAT systems, economists predicted it will never work.

But it worked, because Germans worked hard for that paper money, even if it can not be converted to Gold or Silver or “guaranteed amount of bushels of grain” or this or that product of scarcity (that in the terms of grain, actually provide some purpose).

So does printing more money cause inflation?

Sure it does.

Ask yourself: What does a bank produce?

Actually a bank produces only one thing: loans.

If it does not produce loans, it’s like a factory with no output (lost it’s purpose).

The question is: If the banks fail at their core task, can the state step in, and lend money to citizens that want to create those innovative products = jobs?

Also What is the best way to battle inflation?

Imho it would be:

- a actually working banking system that actually produces loans into the hands of innovative (entrepreneurship) citizens that want to add value

- if the state does not want to take over that role, it needs to force banks to do their job properly

second best fix:

- increase the price for money

- aka increase the price for borrowing money (if something costs nothing it’s not worth anything?) aka increase central bank interest rates on that central bank money (Russia currently has 15.90% Inflation and a central bank interest rate of 9.50% (https://tradingeconomics.com/matrix)

Thatcher did that it was not pretty.

Buying and selling stocks or real estate, is not investment, it’s speculation (not adding value to society in any sense).

#money #alternative #systems #altcoopsys #alternatives #OsOfSociety #OperatingSystemsOfSociety #SystemPhilosophy #dinero #dollar #euro #yen #rubel #sustainability #resilience #complementary #complementarycurrency #cooperation #monetaryreform #financialreform #financialsystemreform #financialcrisis #mortagecrisis #debtcrisis #occupywallsreet #finance #moneysystem #financialsystem #economics #ecologicaleconomics #economy #capitalism #kapitalismus #system #central #bank #inflation #fita #currency #banks #loans #loan #credit #value #adding #democracy

Originally posted at: https://altcoopsys.org/2022/07/22/how-the-modern-fiat-money-system-works-what-causes-inflation/

13 Likes

1 Comments

1 Shares

COMMENT LA BCE S'EST FAIT PIÉGER PAR SA CRÉATION MONÉTAIRE - Élucid

#économie #finance #UE #euro #effondrement

Attendez-vous à une crise comme on n'en a jamais vu.

One person like that

1 Shares

One person like that

Интернет демократизировал знание, блокчейн демократизирует богатство

Одной из причин, по которой многие люди увлекаются миром блокчейна, является то, что это не новый технологический слой, а фундаментально иной инструмент для работы организаций и сообществ.

Главная проблема заключается в том, что без массовой децентрализации мы получаем все больше и больше неравенства между богатыми и бедняками. Поговорим об эволюции общества и централизации для объяснения ценности блокчейна как трансформатора социальных структур.

Взаимоотношения общества с хищниками означает, что защитить что-то сложнее, чем это сделать. Многие века мы были в обществе собирателей-охотников, и было относительно легко защитить наши активы – мы просто носили их с собой.

Но по мере усложнения общества, мы создали больше ценных вещей, и нам нужно было создать больше инструментов для защиты этих вещей.

Это привело к тому, что появились люди, которые могли бы защитить активы, но банковские системы и суверенные государства принципиально выбирали логику насилия.

Это происходило на протяжении многих сотен лет, а потом интернет ускорился, и такая централизация вызвала тревогу.

Таким образом, за довольно короткое время – буквально за последние 10 лет, мы стали высоко централизованным обществом.

Теперь границы поражены, так как у нас есть глобальные монополии. У нас есть пять или шесть компаний, которые владеют тревожным количества данных, богатством и контролем.

Итак, кто же эти интернет-гиганты, построившие, казалось бы, нерушимые глобальные монополии?

В 1996 году, Google запустили как исследовательский проект 2 аспиранта Стэнфордского университета. Скромный старт компании осуществили из гаража друга, но сегодня она стоит около $132 млрд. Вместе с Amazon, Facebook, и Apple, компания накопила так много энергии, что многие верят – она дискредитирует американскую демократию.

Amazon генерирует 30% всех онлайн и оффлайн розничных продаж в США, в то время как Apple является самой ценной в мире фирмой, с рыночной капитализацией $1 трлн.

Google контролирует более 70% глобальной доли рынка поисковой рекламы. Вместе с Facebook, компания выставила из бизнеса большую часть конкурентов по онлайн-рекламе.

Но способность интернет-гигантов контролировать распространяется дальше бизнес-мира. Во всем мире, у многих людей формируется осведомленность о текущих событиях, так или иначе, через Facebook и Google, которые определяют, какую информацию мы видим и потребляем со скрытыми алгоритмами.

Они контролируют, как мы думаем, они контролируют, как мы голосуем, и это довольно страшное пространство, их очень сложно сместить. Мы знаем: сеть – эффективная и мощная, и это было бы невероятно трудно для кого-то - вытеснять Facebook с другой децентрализованной моделью.

Но блокчейн дает возможность ликвидировать эти монополии для создания лучшего, более честного и справедливого общества. Итак, блокчейн – это инфраструктура, которая может позволить централизации двигаться в децентрализованный мир.

Многие говорят о блокчейне как о децентрализованной книге или базе данных, но они упускают суть. Смысл можно найти в создании децентрализованных экономических криптомоделей, таких как второе поколение блокчейнов, например, Ethereum, который теперь считается децентрализованным механизмом выполнения кода или платформой.

Эта концепция была придумана в блоге, в протоколе Fat: интернет первого поколения был построен по линиям тонкого протокола. Но Berners Lee, который создал первый интернет в 1980-х годах, на самом деле не заработал на этом деньги.

Люди, которые построили так называемые «жирные приложения» Google, Facebook и Amazon, извлекают теперь массивные значения из этого слоя жира на тонком протоколе, и зарабатывают деньги.

Существенное различие между началом интернета, технологическими гигантами, что выросли из этого, и возможностями блокчейна, которые открываются сегодня – это то, что блочная цепь позволяет людям создавать жирные протоколы с открытым исходным кодом. Это открытые, прозрачные протоколы, созданные сообществами разработчиков.

Но вместо того, чтобы работать бесплатно, они получили такой экономический стимул для строительства проектов, потому что через токенизацию мы теперь можем владеть цифровой собственностью и создавать токены, представляющие эти протоколы, а также открывать рынки для их торговли.

Поэтому люди с новыми идеями, протоколами и стартапами могут собрать много денег для поддержки строительства их общин с целью развития второго слоя на базе бит интернета.

Здесь есть немного дикого запада в отношении захвата денег, и это, возможно, одна из вещей, что выдвинула концепция ICO.

В прошлом столетии мы наблюдали безумие, а затем крушение dot.com. То, что происходит сейчас, похоже на это событие: генерируются тысячи ICO и возникают связки основных базовых протоколов, которые открыты сообществу, управляемы, полностью децентрализованы и неподвластны никаким центральным организациям или контролирующим лицам. Они будут контролироваться держателями токенов, поэтому они будут победителями. И люди, которые будут выбирать победителей, покупая у них токены, будут влиять на увеличение стоимости этих токенов, в результате чего эти победители выиграют в финансовом плане.

Но в более широком смысле, это должно дать нам более справедливое пространство, где будут не только состоятельные люди и финансовые инвесторы Силиконовой Долины, Сингапура или Лондона, которые зарабатывают большие деньги. Надо демократизировать это пространство.

Как интернет демократизировал знания, блокчейн демократизирует богатство.

Теперь мы можем участвовать в более справедливой системе и токенизированной экономике, где все может быть токенизировано – от футбольных команд до строительства и новых идей, которые могут быть полностью ликвидными и торгуемыми, и люди могут стать собственным Швейцарским банком.

Частный ключ разрывается на двенадцать букв в голове пользователей блокчейна, и они становятся суверенными лицами. Они не нуждаются в огромной системе банковской инфраструктуры или крупной корпорации для управления их богатством, их данными и медицинскими записями.

Таким образом, технология blockchain и токенизация позволят увеличить количество активов, которые могут легко покупаться и продаваться, а для многих людей устранятся предыдущие барьеры

для торговли и инвестирования, что часто было зарезервировано для богатых.

Это также может привести к созданию большого количества фирм, что являются социально ответственными – если стартапы финансируются толпой, то они, скорее всего, будут предлагать услуги, продукты и идеи, в которых «толпа» будет заинтересована в достижении успеха.

Время покажет, насколько далеко будут направлены текущие проекты блокчейн-цепочки, чтобы децентрализировать видение будущего и демократизировать богатство. Но позитивное будущее заключается в том, что в блокчейн-пространстве находится много людей – вот почему мы страстно увлечены этим.

#интернет #демократия #блокчейн #криптовалюты #децентрализация #централизация #контроль #иллюзия #монополия #справедливость #финансы #токен #internet #democracy #blockchain #cryptocurrencies #decentralization #centralization #control #illusion #monopoly #justice #finance #token #lang-ru #lang_ru

Источник

One person like that

Morningstar cuts 'various' drove of Chinese works, moves ops somewhere

The US-based Morning Star said Wednesday that it has cut or relocated hundreds of jobs at its Chinese hub in Shenzhen and is moving its business to other countries.

A financial services company that provides investment trusts and investment research for asset management said in a statement that it employs about 1,000 people in cities in southern China.

Some employees will be transferred to Mumbai, Toronto, Madrid, or Chicago (Global Headquarters) in the coming months. A spokesman for another company added that most of them are involved in "supporting global operations."

In his statement, Morning Star said that the "strategic shift" in China's business was to "fully focus on the domestic market" and that China's service team would not be affected by headcount reductions. ..

"We are in the process of defining a new strategy for the growth of the Chinese market," he said without going into detail.

Bloomberg first reported on the move on Wednesday.As China continues to tighten its privacy and cybersecurity rules, global financial companies operating in China are increasingly concerned that transferring corporate or customer data abroad can be more cumbersome. doing.

Earlier this month, cybersecurity regulators, the world's second-largest economy, announced a set of rules for assessing outbound data from companies doing business in the country starting September 1.

After entering China 20 years ago, Morningstar embarked on global equity research and portfolio management.

credit:the dough roller

2 Likes

#Amazon Hub in #Newark Is Canceled After Unions and Local Groups Object

source: https://www.nytimes.com/2022/07/07/business/economy/amazon-newark-airport-new-jersey.html

It was in part the #company’s prominence in the state that attracted opposition to the project. A report produced by groups seeking to block it pointed out that the number of Amazon facilities in #NewJersey grew to 49 from one between 2013 and 2020, helping to nearly triple the number of warehouse workers in the state, to about 70,000. Over the same period, the average #wage for those workers fell to about $44,000 per year from over $53,000 per year, adjusting for inflation, according to #Labor Department data.

#work #job #finance #economy #politics #problem #news #lobby

5 Likes

The #Uber #whistleblower: I’m exposing a #system that sold people a #lie

source: https://www.theguardian.com/news/2022/jul/11/uber-files-whistleblower-lobbyist-mark-macgann

“The #company approach in these places was essentially to break the #law, show how amazing Uber’s service was, and then change the law. My #job was to go above the heads of city officials, build relations with the top level of #government, and negotiate. It was also to deal with the fallout.”

#economy #startup #money #business #fail #finance #justice #politics #news

2 Likes

1 Shares

Charlene Chu, famed among #China watchers for warning about a debt bubble when at Fitch Ratings, says that pain is only just beginning for credit extended to Chinese #property.

In the wake of #Beijing’s sweeping crackdown on leverage built up in #realestate, China #Evergrande Group and others have defaulted on a slew of bonds. Chu, a senior analyst at Autonomous Research, a division of Sanford C. Bernstein & Co., estimated that “we have 30 companies who’ve defaulted with total liabilities of around $1 trillion.”

While banks have the safeguard of collateral for their loans to developers, “where things could start to get a lot more ugly” is if lenders start revaluing that collateral lower, Chu said in a June 15 interview with the One Decision podcast.

“We’re just so early in this process of these defaults happening, and restructurings usually take quite a long time,” said Chu, who was known at Fitch for warning in the early 2010s over debt risks in the shadow #banking sector. “We haven’t really gotten to the point of saying, ‘OK, well, what really is going to happen with that building?’”

https://www.bloomberg.com/news/articles/2022-07-07/china-property-slide-early-in-game-after-1-trillion-defaults #finance #crisis #economy

The #bank run is burnt into the collective U.S. imagination for good reason. When the Great #Depression hit, the savings of millions of Americans were wiped out when their banks collapsed. That’s why the Federal Deposit Insurance Corp. ( #FDIC) was introduced in 1933. Since then, not a penny of FDIC-insured funds has been lost when banks go under.

It’s a different story when your “bank” is a #cryptocurrency firm. As #crypto prices collapse, customers’ deposits are disappearing with them—or being swiped by the people behind the company. Unregulated markets are looking very much the same now as they did in the 1920s.

#Bitcoin advocates have largely switched away from claiming that the cryptocurrency can function as an actual #currency, mainly due to it still being largely unfeasible to pay for anything in it. Now the claim is that bitcoin is a “store of value”—that is, an asset that won’t lose its worth over time. This has been dramatically shown untrue. More than that, the storekeepers were shoveling the valuables into their own—U.S. dollar-denominated—vaults.

https://foreignpolicy.com/2022/06/21/crypto-regulation-ust-luna-celsius-collapse/ #usa #crisis #economy #tesla #musk #web3 #finance

One person like that

1 Comments

1 Shares

2 Likes

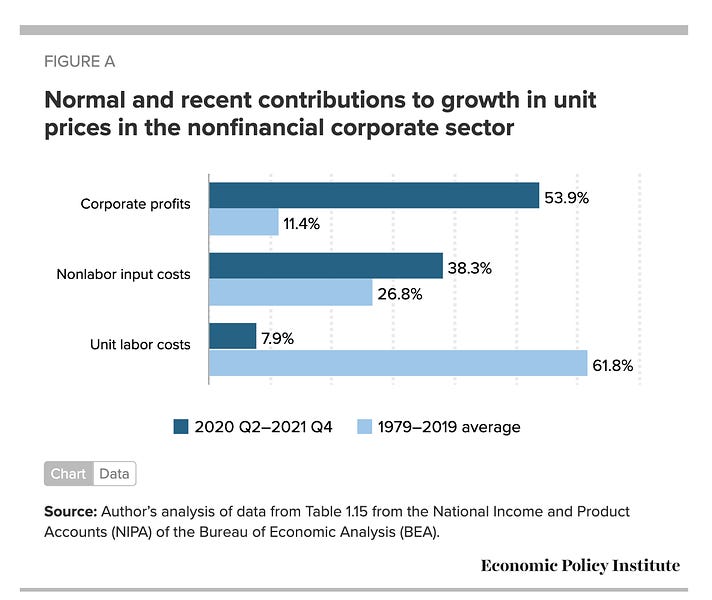

What drives #inflation?

source: https://adamtooze.substack.com/p/chartbook-122-what-drives-inflation

Whereas in recent decades, unit labour costs (wages/productivity) have accounted for 62 percent of price increases and corporate profits for only 11.4 percent, with non-labour input costs (like energy) making up the rest, since 2020 the balance has been reversed. Since the COVID shock in 2020, wages have accounted for less than 8 percent of US price increases, as against corporate profits which accounted for almost 54 percent. Input costs, notably energy, have accounted for 38 percent.

#economy #prices #profit #capitalism #politics #news #money #finance

3 Likes

#Louisiana’s #insurance #market is collapsing, just in time for #hurricane season

source: https://grist.org/housing/louisiana-homeowner-insurance-hurricane-season/

A few months earlier, a major insurance company called Lighthouse had gone bankrupt, leaving almost 30,000 homeowners in the state without storm coverage. The company went under thanks to last year’s Hurricane Ida, which led to $400 million in damage claims, far more money than the company had on hand. It had been up to Donelon to find a new company to take over these abandoned policies, but no other #company wanted them. In fact, other companies were fleeing the state en masse.

#usa #capitalism #finance #security #problem #money #news #economy #environment #damage #crash #weather

2 Likes

Thousands protest in #Madrid against #NATO #summit

source: https://www.reuters.com/world/europe/thousands-protest-madrid-against-nato-summit-2022-06-26/

"Tanks yes, but of beer with tapas," sang demonstrators, who claimed an increase in #defence spending in #Europe urged by NATO was a #threat to #peace.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UFRBLZMM75ME5MCV2BXH5ZUQDI.jpg)

2 Likes

3 Comments

3 Likes

2 Comments